The Threat Of Western Central Bank Digital Currencies, Amid Information War

By Sundance

After my latest outline on the looming probability of a dollar based Central Bank Digital Currency (CBDC), I said:

I hate to say this, but most people really don’t care. For some, the issue is esoteric, abstract, and difficult to comprehend. For others, there is a massive blanket of comfortable ambivalence until the consequences hit. For the few who understand, this is extremely troubling.

Then I step back, breathe and reevaluate my ability to communicate. A few recent comments have me looking for something, anything, that will help people understand the scope and breadth of what I am trying to communicate, and the challenge therein. Some comments to consider:

#1 - I don’t know, this is way over my head, and I consider myself at least somewhat intelligent and informed. Other than a few twenties I keep in my wallet, all money of consequence in my life is already just digits in computer networks as far as I can perceive. I never actually see a check for my wages, much less any dead presidents.

Not that I disagree, I just don’t understand. I’m at a loss as to why this is so qualitatively different as far as my financial security goes. Maybe it’s because I’m a resident of Illinois and have some sort of Stockholm Syndrome from knowing they can already, and do, raise my taxes – as much as they want, any time they want – and there is nothing to stop them.

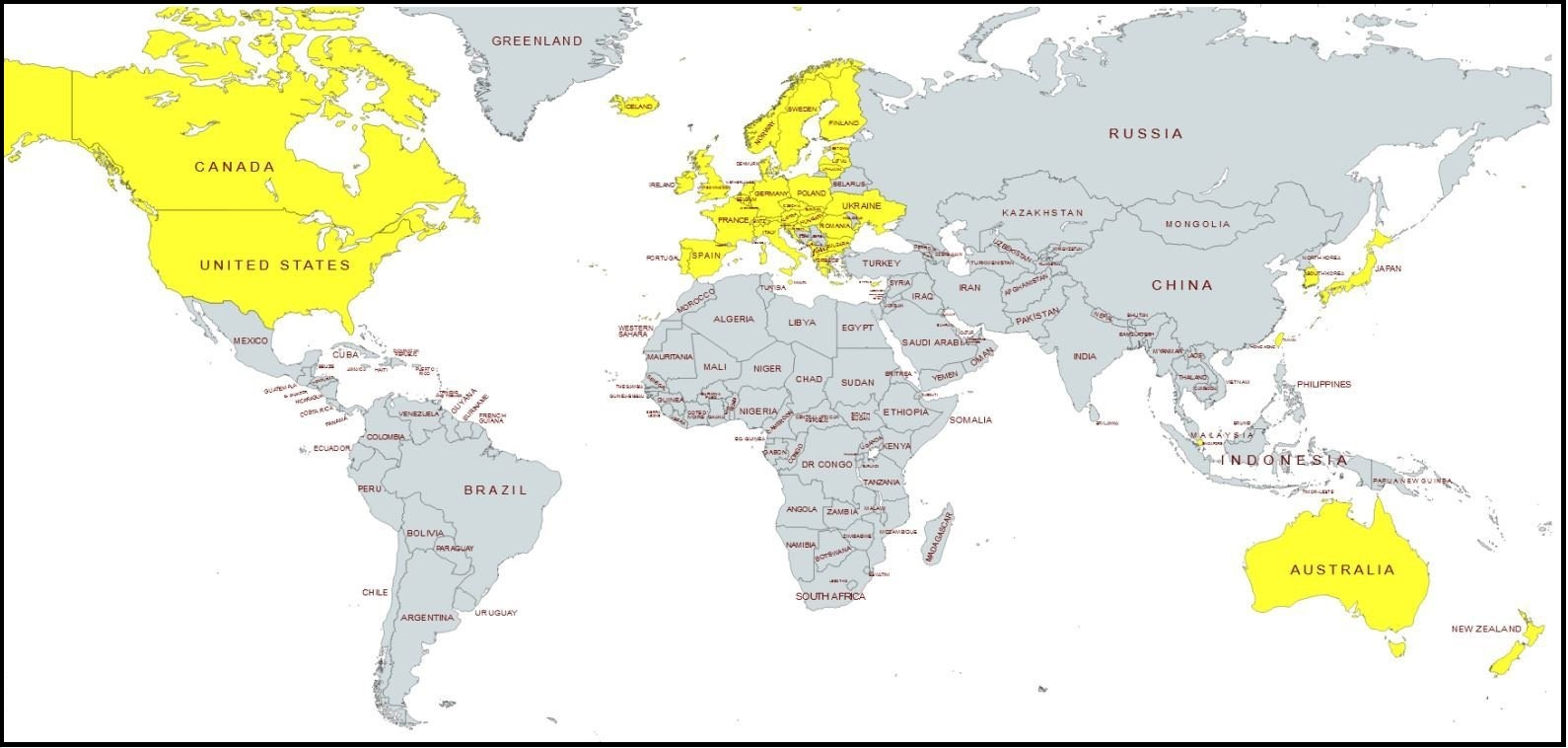

#2 - I apologize for this stupid question, but I’m confused. How do the grey countries fit into this digital money and “world order” Pippa refers to?

Pippa states “But what I see our superpowers introducing digital currency, the Chinese were the first the US is on the brink, I think of moving in the same direction the Europeans have committed to that as well.”

China is grey on the map, as is Russia. If we, the mapped yellow USA, are being boxed in by the Russian sanctions how is it China is grey yet they were the first to introduce a digital currency? These insane, drunk with power “superpowers” – is their goal to color the entire world map yellow with the SWIFT network digital coin to control the entire world?

You come here for understanding the world that exists, not the one we may hope to exist. If you are confused, I need to do a better job. I will start first with some lesser known information.

Ever since the western sanctions against Russia were created, an entire new black market of finance has been created in the “grey zone” that circumvents the sanctions and assists the people trapped by them.

Only a handful of people have a full understanding of what’s really happening. Within the yellow zone, this information and understanding is virtually unattainable. And, you cannot get this level of comprehension from a keyboard safely in your home. You have to put your boots on the ground, take risks and see exactly how it works.

Russian Sanctions Were Created To Wall-In The West

There are networks of people who operate in various places that create proactive financial mechanisms for what you might call, “financial preppers.”

These people and groups set up bank accounts in foreign countries for you; they organize addresses (needed), phone numbers (needed), and create accounts that you can access that are outside the control of the dollar-based financial system. You can even get an official passport in the process.

These people sell hardware to support the phone numbers (digital IDs), which are completely different from what exists behind the wall of the yellow zone. How many Americans know that an iPhone15 sold in the US is completely different from an iPhone15 sold outside the yellow zone? Meaning, the internal hardware is different. How many Americans know that? How many Americans know that an iPhone15 sold inside the US has different originating software than an iPhone15 sold outside the US?

How many people know that when you purchase one of these “ghost phones” the data network automatically identifies the disparity when the phone crosses into the yellow zone, and shortly thereafter the cellular network transmits a software update to bring the “ghost phone” into the USA (yellow zone) compliance? How many Americans know phone apps and internal app functions can exist on phones outside the yellow zone that do not exist inside the yellow zone?

Example: Use a ghost phone, and you can access a digital wallet in Telegram, and transmit funds to other Telegram users. However, use a USA compliant phone and the service is, “not available in your area.”

Why? It’s about control. If you don’t update the software, the function exists inside the yellow zone. However, update the software and the function disappears.

Another real-life example is the story of the Apple Watch, Series 9, was found to have violated patent technology and banned for sale in the USA. To get into legal compliance, Apple transmitted a remote software update disabling the function of the patent technology in the USA.

Again, for emphasis, only in the USA. Bring your non-compliant Series-9 into the range of a Wi-Fi network and bingo auto-compliance. I mention this story only to highlight a modern compliance capability that many people do not know exists.

Western Zone Tech Devices Are Different From Identical Tech Devices Sold Outside The Zone

Technology is intertwined with Central Bank Digital Currencies. Tech companies are regulated by the US/Western government, and the tech companies have to comply. The regulatory compliance is part of the process of control. There are regulatory walls around us that most do not understand. The same regulatory principle applies to finance and banking. Hence, the origination motive of the yellow zone wall, built under the auspices of Russian sanctions.

When The Western Central Bank Digital Currency System Begins, Cryptocurrency Will Be Blocked & Made Unlawful In The West

Yes, Cryptocurrency will be banned. Crypto is not technically a currency, it is a barter based on trust. However, at a certain point (origination or end) crypto must have the ability to transfer into currency value. Dollars (or another currency) are needed to purchase Bitcoin and eventually sold or exchanged for Dollars (or another currency). This process is where crypto gets blocked.

Ownership of Crypto may not be unlawful, but any effort to use Crypto as an alternate digital currency to exchange value will be unlawful once the dollar based CBDC is launched. A fully implemented Government controlled central bank digital currency will not allow competition. Alternate cryptocurrency will be banned. Without any doubt!

Back to the original questions:

China is grey on the map, as is Russia. If we, the mapped yellow USA, are being boxed in by the Russian sanctions how is it China is grey yet they were the first to introduce a digital currency?

The gray zone can trade amongst themselves however they want; the yellow zone (West) has no capability to stop them. Ex. if Russia wants to trade 1,000 barrels of oil with China for 100 boxes of intel microchips, they can. Or if China and Russia want to exchange digital yen for digital rubles, they can; the West cannot stop them.

However, if China wants to interact with a yellow zone member, the yellow zone financial rule makers have rules. China would have to be compliant with a dollar based CBDC to exchange value within the yellow zone.

Similarly, if you want to exchange a bushel of corn for 10 dozen eggs with your neighbor, you can; there is no mechanism to stop you. However, if you need to pay your mortgage you will have to be compliant with a dollar based CBDC to exchange value, i.e., pay your bill.

all money of consequence in my life is already just digits in computer networks as far as I can perceive. … I’m at a loss as to why this is so qualitatively different as far as my financial security.

This is the common mistake that most people make. There is a big difference between “electronic transactions” of dollars, and the existence of a “digital dollar.” Let me give you a metaphor using a casino as the reference.

Current System: You go to the casino window and exchange $10,000 dollars for poker chips valued at $10,000. You give the teller $10,000 in cash, banker’s check, money order, a credit card or debit card transaction, and the teller gives you chips worth $10,000 in that casino. You can use the chips gambling and perhaps win more chips. Return to the window with $12,000 in casino chips and the teller exchanges the chips for $12,000 dollars, cash or check or deposit into your electronic card.

You meet a man in the casino willing to give you his fancy Rolex watch in exchange for $5,000. You give the man $5,000 worth of your poker chips, and he gives you his Rolex watch. That man can then go to the teller window and exchange the chips for $5,000 in cash. You have the watch.

Digital Dollar System – You go to the teller window and produce your bank card containing a digital dollar balance. You exchange $10,000 worth of your digital dollars for $10,000 dollars’ worth of poker chips. Except this time, with a digital dollar, each poker chip has your fingerprint on it. You spend or bet your poker chips, and each chip you win also arrives to you with your fingerprint on it. You win $12,000 dollars. You return to the window with $12,000 in chips, each with your fingerprint, and the teller uploads your card with $12,000 digital dollars.

You meet a man in the casino willing to give you his fancy Rolex watch in exchange for $5,000. But, you cannot give the man your poker chips because they are unique to you and carrying your fingerprint. If he takes your fingerprint poker chips to the window, his fingerprint does not match the chip, his request for $5,000 in digital dollars would be denied. He cannot sell you his watch. The digital fingerprint limits your transactional capability.

[If he was planning to sell his watch for $5,000 in order to purchase a motorcycle worth $5,000, it is possible for you to purchase the motorcycle, exchange it for his watch and then carry on. However, the motorcycle would be digitally registered to you, and you would be digitally registered to the motorcycle. A reconciliation process is needed.]

A digital dollar creates a unique ID attached to that digital dollar. Ultimately, the central bank that issues the digital dollar controls what the digital ID can do (that’s you), and what those digital dollars can be used for (what you can do).

Digital dollars can be blocked from gun purchases, and digital IDs can be used to stop unapproved users from purchasing guns; or a gas guzzling SUV, or a house that’s too big, or the non-compliant fridge, or whatever.

Sellers of goods (or information) can have their IDs banned from receiving digital dollars, just as VISA and MasterCard blocked sellers of guns from accessing their electronic transaction system. With digital dollars, “demonetization”, an alarmingly familiar modern term, can become a function of a financial regulation system. “Debanking” another alarmingly familiar term, also becomes much easier.

Ultimately, a dollar-based US-Central Bank Digital Currency, IE a “digital dollar,” is about control. Every transaction has a unique digital fingerprint, and every digital dollar can be traced by the IRS to the digital ID associated with it.

There is a big difference between the current electronic funds system and tomorrow’s digital dollar